In 2026, health insurance isn’t just a “nice to have.” Medical costs keep rising, hospital bills can shock even well-planned households, and a single emergency can derail your savings. The hard part is that many people buy a health insurance plan based on the lowest premium—and later discover gaps when they need the coverage most.

This guide breaks down how to choose health insurance the smart way, focusing on value, clarity, and real protection—so you can avoid overpaying for health insurance without under-insuring yourself.

Key Health Insurance Terms (Explained Simply)

Premium: The amount you pay regularly (monthly/quarterly/yearly) to keep the policy active.

Deductible / Excess: The amount you pay from your pocket before the insurer starts paying. (A higher health insurance deductible usually lowers your premium.)

Copay / Coinsurance: A fixed amount (copay) or percentage (coinsurance) you pay for certain services, even after coverage starts.

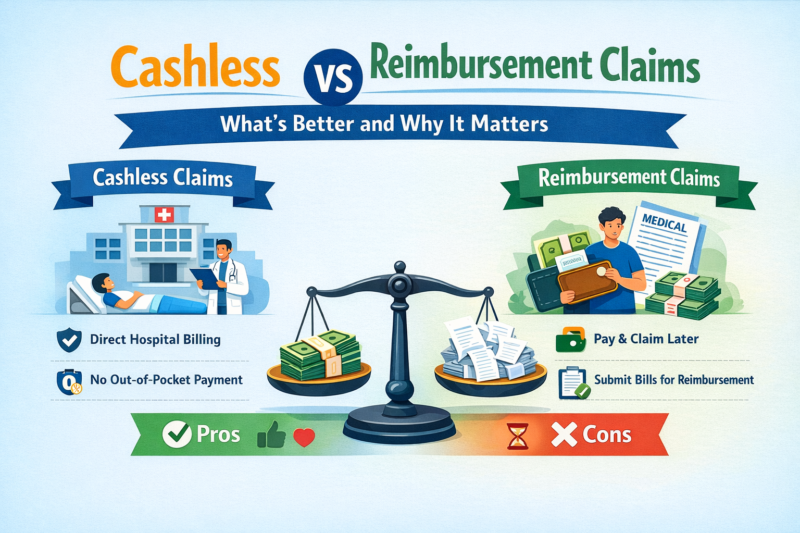

Network / Cashless hospitals: Hospitals tied to the insurer where you can use cashless treatment (subject to approvals). Out-of-network often means you pay first and claim later.

Waiting periods: A time window during which certain claims aren’t covered (common for pre-existing conditions, maternity, and specific procedures).

Exclusions: Items the policy will not cover—ever or during certain periods.

Claim settlement / approvals: How claims are processed, approved, and paid (especially important for cashless hospitalizations).

How to Choose the Right Plan Without Overpaying

1) Start with your real needs (not what an agent suggests)

Your “best” plan depends on your profile:

- Age and family size

- Any chronic conditions (diabetes, asthma, blood pressure)

- Planned events (pregnancy, surgeries)

- Frequency of doctor visits/medicines

- Travel habits (domestic/international)

- Employer coverage gaps (if you have corporate insurance)

If you rarely visit hospitals, you may prioritize strong hospitalization coverage and a manageable deductible. If you have frequent outpatient expenses, check whether OPD benefits are meaningful (often they are limited and can be pricey).

2) Pick a practical coverage amount

Don’t choose coverage purely based on fear—but don’t undercut it either. As a rough approach:

- Young single: enough to cover a major hospitalization in your city

- Family: higher coverage because multiple people can claim

- Parents/seniors: higher risk → higher coverage and careful terms

The goal is to cover “big events” that can destroy savings. Small bills should not dictate your whole policy.

3) Compare total cost, not just the premium

This is where people overpay—or under-cover—without realizing it. Look at:

- Premium + deductibles/excess

- Copay/coinsurance amounts

- Limits on room rent and ICU charges

- Sub-limits on procedures (if any)

- Claim-related deductions (non-payables)

A cheaper premium with a strict room rent cap can cost you far more during hospitalization because many hospitals price packages based on room category.

[Insert comparison table here]

4) Check cashless network and the claim process

A strong network matters if you want convenience. Before you buy:

- Search for hospitals near your home and workplace

- Understand the cashless process: pre-authorization, timelines, required documents

- Ask how reimbursement works if cashless isn’t available

A plan is only as good as how smoothly it pays.

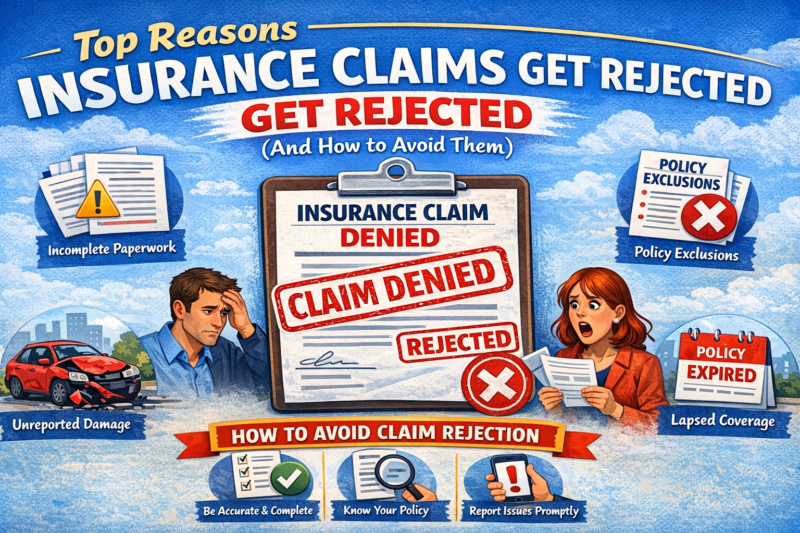

5) Read exclusions and waiting periods like it’s a contract (because it is)

Key things to verify:

- Pre-existing condition waiting period (how long until covered)

- Maternity waiting period (often 1–4 years)

- Specific disease/procedure waiting period

- Permanent exclusions (cosmetic procedures, certain treatments, etc.)

If you skip this step, you’re not buying insurance—you’re buying hope.

6) Be selective with add-ons (riders)

Add-ons can be worth it, but don’t stack them blindly. Consider add-ons only if they match your risk:

- Critical illness: useful for income disruption, but read definitions carefully

- Hospital cash: can help with incidental costs

- Accident cover: often good value if priced fairly

Skip add-ons if they duplicate benefits you already have (through employer plans or separate policies).

7) Check service quality, not just marketing

Look for signs of a reliable insurer:

- Clear policy wording and transparent disclosures

- Easy customer support access

- Smooth digital claim tracking

- Consistent communication during claims

A slightly higher premium can be worth it if it saves you stress and delays during emergencies.

[Insert CTA here: get quotes]

Mini Examples: Choosing Without Guesswork

Profile 1: Young single professional

Priorities:

- Solid hospitalization coverage

- Higher deductible to reduce premium (if you have savings for small costs)

- Strong cashless network near home/work

Avoid: - Paying extra for benefits you won’t use (heavy OPD add-ons, unnecessary riders)

Profile 2: Family with kids (and possible parent coverage)

Priorities:

- Higher overall coverage (more claim potential)

- Low or manageable copay

- Good pediatric and maternity terms (if relevant)

- Clear exclusions and waiting periods

Avoid: - Policies with strict room caps and heavy sub-limits that trigger big out-of-pocket costs

Common Mistakes People Make

- Buying only based on the lowest premium

- Ignoring the health insurance deductible and copay rules

- Not checking hospital network coverage

- Skipping exclusions and waiting periods

- Underinsuring because “I’m healthy” (until you’re not)

- Overinsuring with expensive add-ons that rarely pay out

Quick Health Insurance Checklist

- Coverage amount fits your city and family needs

- Premium + deductible + copay make sense together

- No harsh room rent caps or hidden sub-limits

- Nearby hospitals are in-network for cashless

- Waiting periods are acceptable for your situation

- Exclusions are clearly understood

- Claim process is simple and transparent

FAQ

Should I choose a higher deductible to reduce premium?

Only if you can comfortably pay the deductible in an emergency. Otherwise, a cheaper premium can become expensive at the worst time.

Is cashless insurance always better than reimbursement?

Cashless is more convenient, but what matters is how smoothly approvals happen and whether your preferred hospitals are in the network.

How can I avoid overpaying for health insurance?

Match coverage to your real risk, compare total cost (not premium alone), and skip riders that don’t fit your needs.

Choosing the right health insurance plan is less about finding a “perfect” policy and more about avoiding costly surprises. If you focus on total cost, network access, exclusions, and claim experience, you’ll get stronger protection—without paying for features you don’t need.

Disclaimer: This is not financial advice. Do your own research or speak to a licensed advisor before making insurance decisions.